As filed with the U.S. Securities and Exchange Commission on September 10, 2021.

Securities Act File No.

File No. 814-01431

Initial filing of a registration statement on Form N-2 for closed-end investment companies

September 10, 2021

Published on September 10, 2021

☐ |

Check box if the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans. |

☒ |

Check box if any securities being registered on this Form will be offered on a delayed or continuous basis in reliance on Rule 415 under the Securities Act of 1933 (“Securities Act”), other than securities offered in connection with a dividend reinvestment plan. |

☐ |

Check box if this Form is a registration statement pursuant to General Instruction A.2 or a post-effective amendment thereto. |

☐ |

Check box if this Form is a registration statement pursuant to General Instruction B or a post-effective amendment thereto that will become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act.

|

☐ |

Check box if this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction B to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act.

|

☐ |

when declared effective pursuant to Section 8(c) of the Securities Act. |

☐ |

This [post-effective] amendment designates a new effective date for a previously filed [post-effective amendment] [registration statement]. |

☐ |

This Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, and the Securities Act registration statement number of the earlier effective registration statement for the same offering is: .

|

☐ |

This Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, and the Securities Act registration statement number of the earlier effective registration statement for the same offering is: .

|

☐ |

This Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, and the Securities Act registration statement number of the earlier effective registration statement for the same offering is: .

|

☐ |

This Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, and the Securities Act registration statement number of the earlier effective registration statement for the same offering is: .

|

☐ |

Registered Closed-End Fund (closed-end company that is registered under the Investment Company Act of 1940 (“1940 Act”)). |

☒ |

Business Development Company (closed-end company that intends or has elected to be regulated as a business development company under the 1940 Act). |

☐ |

Interval Fund (Registered Closed-End Fund or a Business Development Company that makes periodic repurchase offers under Rule 23c-3 under the 1940 Act). |

☐ |

A.2 Qualified (qualified to register securities pursuant to General Instruction A.2 of this Form). |

☐ |

Well-Known Seasoned Issuer (as defined by Rule 405 under the Securities Act). |

☒ |

Emerging Growth Company (as defined by Rule 12b-2 under the Securities Exchange Act of 1934 (“Exchange Act”). |

☐ |

If an Emerging Growth Company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of Securities Act.

|

☒ |

New Registrant (registered or regulated under the 1940 Act for less than 12 calendar months preceding this filing). |

Title of securities being registered |

| |

Proposed Maximum

Aggregate Offering price(1)

|

| |

Amount of

Registration fee(1)

|

Common shares of beneficial interest, $0.01 par value per share

|

| | $2,000,000,000 |

| | $218,200 |

(1) |

Estimated pursuant to Rule 457(o) under the Securities Act of 1933 solely for the purpose of determining the registration fee. |

• |

We have no prior operating history and there is no assurance that we will achieve our investment objective. |

• |

This is a “blind pool” offering and thus you will not have the opportunity to evaluate our investments before we make them. |

• |

You should not expect to be able to sell your shares regardless of how we perform. |

• |

You should consider that you may not have access to the money you invest for an extended period of time. |

• |

We do not intend to list our shares on any securities exchange, and we do not expect a secondary market in our shares to develop prior to any listing. |

• |

Because you may be unable to sell your shares, you will be unable to reduce your exposure in any market downturn. |

• |

We intend to implement a share repurchase program, but only a limited number of shares will be eligible for repurchase and repurchases will be subject to available liquidity and other significant restrictions.

|

• |

An investment in our Common Shares is not suitable for you if you need access to the money you invest. See “Suitability Standards” and “Share Repurchase Program.”

|

• |

We cannot guarantee that we will make distributions, and if we do we may fund such distributions from sources other than cash flow from operations, including, without limitation, the sale of assets, borrowings, or return of capital, and we have no limits on the amounts we may pay from such sources.

|

• |

Distributions may also be funded in significant part, directly or indirectly, from temporary waivers or expense reimbursements borne by the Adviser or its affiliates, that may be subject to reimbursement to the Adviser or its affiliates. The repayment of any amounts owed to the Adviser or its affiliates will reduce future distributions to which you would otherwise be entitled.

|

• |

We expect to use leverage, which will magnify the potential for loss on amounts invested in us. |

• |

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our Common Shares less attractive to investors.

|

• |

We intend to invest primarily in securities that are rated below investment grade by rating agencies or that would be rated below investment grade if they were rated. Below investment grade securities, which are often referred to as “junk,” have predominantly speculative characteristics with respect to the issuer’s capacity to pay interest and repay principal. They may also be illiquid and difficult to value.

|

| | |

Price to the

Public(1)

|

| |

Proceeds to Us,

Before Expenses(2)

|

|

Maximum Offering(3)

|

| | $2,000,000,000 |

| | $2,000,000,000 |

Class S Shares, per Share

|

| | $25.00 |

| | $500,000,000 |

Class D Shares, per Share

|

| | $25.00 |

| | $500,000,000 |

Class I Shares, per Share

|

| | $25.00 |

| | $500,000,000 |

Class F Shares, per Share

|

| | $25.00

|

| | $500,000,000

|

Minimum Offering

|

| | $100,000,000

|

| | $100,000,000

|

(1) |

The price per share shown will apply until funds are released to us from the escrow account. Thereafter, shares of each class of our Common Shares will be issued on a monthly basis at a price per share equal to the NAV per share for such class. |

(2) |

No upfront sales load will be paid with respect to Class S shares, Class D shares, Class I shares or Class F shares; however, if you buy Class S shares, Class D shares or Class F shares through certain financial intermediaries, they may directly charge you transaction or other fees, including upfront placement fees or brokerage commissions, in such amount as they may determine, provided that they limit such charges to a 3.5% cap on NAV for Class S shares, a 2.0% cap on NAV for Class D shares and a 2.0% cap on NAV for Class F shares. Selling agents will not charge such fees on Class I shares. We will also pay the following shareholder servicing and/or distribution fees to the Managing Dealer and/or a participating broker, subject to Financial Industry Regulatory Authority, Inc. (“FINRA”) limitations on underwriting compensation: (a) for Class S shares, a shareholder servicing and/or distribution fee equal to 0.85% per annum of the aggregate NAV as of the beginning of the first calendar day of the month for the Class S shares, (b) for Class D shares, a shareholder servicing fee equal to 0.25% per annum of the aggregate NAV as of the beginning of the first calendar day of the month for the Class D shares, and (c) for Class F shares, a shareholder servicing and/or distribution fee equal to 0.50% per annum of the aggregate NAV as of the beginning of the first calendar day of the month for the Class F shares, in each case, payable monthly. No shareholder servicing or distribution fees will be paid with respect to the Class I shares. The total amount that will be paid over time for other underwriting compensation depends on the average length of time for which shares remain outstanding, the term over which such amount is measured and the performance of our investments. We will also pay or reimburse certain organization and offering expenses, including, subject to FINRA limitations on underwriting compensation, certain wholesaling expenses. See “Plan of Distribution” and “Estimated Use of Proceeds.” The total underwriting compensation and total organization and offering expenses will not exceed 10% and 15%, respectively, of the gross proceeds from this offering. Proceeds are calculated before deducting shareholder servicing or distribution fees or organization and offering expenses payable by us, which are paid over time. |

(3) |

The table assumes that all shares are sold in the primary offering, with 1/4 of the gross offering proceeds from the sale of Class S shares, 1/4 from the sale of Class D shares, 1/4 from the sale of Class I shares and 1/4 from the sale of Class F shares. The number of shares of each class sold and the relative proportions in which the classes of shares are sold are uncertain and may differ significantly from this assumption. |

• |

a gross annual income of at least $70,000 and a net worth of at least $70,000, or |

• |

a net worth of at least $250,000. |

• |

meets the minimum income and net worth standards established in the investor’s state; |

• |

can reasonably benefit from an investment in our Common Shares based on the investor’s overall investment objectives and portfolio structure; |

• |

is able to bear the economic risk of the investment based on the investor’s overall financial situation, including the risk that the investor may lose its entire investment; and |

• |

has an apparent understanding of the following: |

• |

the fundamental risks of the investment; |

• |

the lack of liquidity of our shares; |

• |

the background and qualification of our Adviser; and |

• |

the tax consequences of the investment. |

Q: |

What is HPS Corporate Lending Fund (“HLEND”)? |

A: |

HLEND (or the Fund) is a new fund externally managed by HPS Investment Partners, LLC (“HPS” or the “Adviser”) that seeks to invest primarily in newly originated senior secured debt and other securities of private U.S. companies within the middle market and upper middle market. We are a Delaware statutory trust and a non-diversified, closed-end management investment company that intends to elect to be regulated as a business development company (“BDC”) under the Investment Company Act of 1940, as amended (the “1940 Act”). We also intend to elect to be treated as a regulated investment company (“RIC”) under the Internal Revenue Code of 1986, as amended (the “Code”).

|

Q: |

Who is HPS Investment Partners, LLC? |

A: |

HPS is a leading global alternative investment manager with $68 billion of total assets under management as of March 31, 2021. HPS invests primarily in non-investment grade credit and manages various strategies across the capital structure that include privately negotiated senior secured debt and mezzanine investments, syndicated leveraged loans and high yield bonds, asset-based leasing and private equity. Established in 2007, HPS has approximately 160 investment professionals and over 400 total employees and is headquartered in New York with eleven additional offices globally. HPS was established as a unit of Highbridge Capital Management, LLC (“HCM”), a subsidiary of J.P. Morgan Asset Management (“JPMAM”). In March 2016, the principals of HPS acquired HPS from JPMAM, which retained HCM’s hedge fund strategies. In June 2018, affiliates of Dyal Capital Partners, a division of Neuberger Berman, made a passive minority investment in HPS.

|

Q: |

What is your investment objective? |

A: |

Our investment objective is to generate attractive risk adjusted returns, predominately in the form of current income, with select investments exhibiting the ability to capture long-term capital appreciation.

|

Q: |

What is your investment strategy? |

A: |

Our investment strategy focuses primarily on newly originated, privately negotiated senior credit investments in high-quality, established middle market and upper middle market companies and, in select situations, companies in special situations. We use the term “upper middle market companies” to generally mean companies with earnings before interest expense, income tax expense, depreciation and amortization (or “EBITDA”) between $50 million to $350 million annually at the time of investment. We may from time to time invest in smaller or larger companies if the opportunity presents attractive investment characteristics and risk adjusted returns. While our investment strategy primarily focuses on companies in the United States, we also intend to leverage HPS’s global presence to invest in companies in Europe, Australia and other locations outside the U.S., subject to compliance with BDC requirements to invest at least 70% of assets in “eligible portfolio companies.” In addition to corporate level obligations, our investments in these companies may also opportunistically include private asset-based financings such as equipment financings, financings against mission-critical corporate assets and mortgage loans. We may also selectively make investments that represent equity in portfolios of loans, receivables or other debt instruments. We may also participate in programmatic investments in partnership with one or more unaffiliated banks or other financial institutions, where our partner assumes senior exposure to each investment, and we participate in the junior exposure.

|

1 |

Data as of March 31, 2021. HPS statistics include investments across Core Senior Lending, Specialty Direct Lending and Mezzanine strategies.

|

Q: |

What types of investments do you intend to make? |

A: |

Under normal circumstances, we will invest at least 80% of our total assets (net assets plus borrowings for investment purposes) in credit and credit-related instruments issued by corporate issuers (including loans, notes, bonds and other corporate debt securities).

|

Q: |

What is an originated loan? |

A: |

An originated loan is a loan where we lend directly to the borrower and hold the loan generally on our own or in a small group with other HPS advised funds and accounts and/or third-party investors. This is distinct from a syndicated loan, which is generally originated by a bank and then syndicated, or sold, in several pieces to other investors. Originated loans are generally held until maturity or until they are refinanced by the borrower. Syndicated loans often have liquid markets and can be traded by investors.

|

Q: |

Why do you intend to invest in liquid credit investments in addition to originated loans? |

A: |

We expect the allocation to liquid credit investments within the Fund’s portfolio (i) to provide the Fund with sufficient liquidity in order to meet the Fund’s share repurchase requirements, and (ii) to seek attractive investment returns prior to investing subscription proceeds into newly originated loans.

|

Q: |

What relative competitive strengths does the Adviser offer? |

A: |

HPS is a leading global, credit-focused alternative investment firm that seeks to provide creative capital solutions and generate attractive risk-adjusted returns for its clients. The scale and breadth of HPS’s platform offers the flexibility to invest in companies large and small across the capital structure through both standard and highly customized structures. At its core, HPS shares a common thread of intellectual rigor and investment discipline that enables it to create value for its clients, who have entrusted HPS with approximately $68 billion of assets under management as of March 31, 2021.

|

• |

Breadth of HPS’s Credit Investment Platform. HPS is a global investment firm with strategies that seek to capitalize on credit opportunities across the capital structure. As a multi-strategy credit platform, seeking opportunities across both private and public credit, HPS employs an open-architecture framework under which investment teams can apply shared knowledge and insights when evaluating new investment opportunities. HPS’s team of approximately 160 investment professionals managed approximately $68 billion across multiple strategies focusing on non-investment grade corporate credit as of March 31, 2021. HPS believes that its multi-strategy approach provides a unique vantage point to evaluate relative value and better positions the firm to provide borrowers with a comprehensive and diverse set of potential financing solutions, which may enable the Fund to see more investment opportunities. |

• |

Scaled Capital with an Ability to Speak for the Full Debt Quantum. Scaled capital has been a key factor in enabling previous funds managed by HPS to access attractive potential investment opportunities. The scale of HPS’s corporate lending platform, including managed accounts and similar investment vehicles, provides the capacity to commit to loans of $500 million to $1 billion, or greater. HPS believes that there are a finite number of competitors who can provide and solely hold investments of this size. For borrowers in the upper end of the middle market, who value confidentiality, efficiency and execution certainty, this capability can be very differentiating and drive investment opportunities. Additionally, due to favorable competitive dynamics associated with fewer capital providers with the ability to deliver scaled capital solutions, HPS believes that it has, to date, been successful in capturing attractive returns relative to the generally lower risk profile of larger, more diversified borrowers. HPS also believes that being the sole or majority investor in a debt tranche also provides the Fund with enhanced downside protection via enhanced control over covenants and loan structure. |

• |

Focus on the Upper Middle Market. HPS’s corporate lending strategy generally targets the upper end of the middle market. As HPS believes that the market is in the later stages of the existing credit cycle, HPS intends to position the portfolio by primarily focusing on larger, more resilient companies that generally generate $50 million to $350 million of EBITDA annually. HPS believes that the upper end |

6 |

Data as of March 31, 2021. HPS statistics include investments across Core Senior Lending, Specialty Direct Lending and Mezzanine strategies.

|

• |

Proven Ability to Source Non-Sponsor Investments. HPS believes its non-sponsor lending capabilities sets its platform apart from many of its peers. While the vast majority of peers focus exclusively on lending to private equity owned businesses, HPS has historically sourced approximately 50% – 60% of its investments from non-sponsor borrowers (which are non-private-equity-backed businesses) by building a strong relationship network across a breadth of companies, management teams, banks, debt advisors and other financial intermediaries. HPS believes its non-sponsor tilt significantly reduces the level of competitive intensity and allows it to focus on structuring improved economics, stricter financial covenants and stronger loan documentation. In addition, the direct dialogue with management teams results in a better understanding of the underlying borrowers and better positioning to actively manage investments throughout their life. While HPS is principally focused on the non-sponsor channel, its exposure to sponsor transactions tends to increase in times of public market dislocation (when certainty of capital and speed of execution with a single counterparty is often sought after and highly valued). The ability to flex in and out of both sponsor and non-sponsor markets will allow the Fund to remain nimble across different market dynamics. |

• |

Ability to Navigate Complex Investment Opportunities. HPS believes that its willingness to embrace complexity, such as complicated business models, esoteric underlying collateral, strained capital structures, and/or timing pressures, is a key differentiating factor relative to its competitors. HPS believes that perceived risk is often mispriced by the market in more complex situations, which can result in disproportionate return opportunities for the smaller number of willing lenders with the requisite expertise to analyze and finance these investments. It has been HPS’s experience that these complicated transactions are often less competitive given the extra work, level of analysis and structuring required and therefore, borrowers particularly value the ability to execute and are willing to pay a premium for it. HPS believes that complexity can be effectively addressed through a combination of incremental effort, creative structuring and compensatory pricing, resulting in opportunities that often can offer attractive, uncorrelated returns for the Fund. |

• |

Emphasis on Capital Preservation. Capital preservation is a core component of HPS’s investment philosophy. In addition to its focus on stable, established middle and upper middle market companies, HPS employs a highly selective and rigorous “private equity like” diligence and investment evaluation process focused on identification of potential risks. HPS believes tight credit structuring is a fundamental part of the risk and recovery calculus, as the illiquidity in private credit means that secondary market liquidity is not a reliable risk mitigant. HPS has also built a deep bench of restructuring, workout and value enhancement professionals with an average of 28 years of workout experience, who work on an integrated basis to actively manage each investment throughout its life. |

Q: |

What is the market opportunity? |

A: |

Private credit as an asset class has grown considerably since the global financial crisis of 2008, and it is estimated that global commitments to private debt represented more than $1 trillion as of the end of 20203. We expect this growth to continue and, along with the factors outlined below, to provide a robust backdrop to what HPS believes will be a significant number of attractive investment opportunities aligned to our investment strategy.

|

• |

Senior Secured Loans Offer Attractive Investment Characteristics. HPS believes that senior secured loans benefit from their relative priority position, typically sitting as the most senior obligation in an issuer’s capital structure, often with a direct security interest in the issuer’s (or its subsidiaries’) assets. |

3 |

Source: Preqin as of December 31, 2020.

|

• |

Regulatory Actions Continue to Drive Demand towards Private Financing. The direct lending market has seen notable growth and has become a viable alternative solution for middle to upper middle market borrowers seeking financing capital. Global regulatory actions that followed the 2008 financial crisis have significantly increased the cost of capital requirements for commercial banks, limiting the willingness of commercial banks to originate and retain illiquid, non-investment grade credit commitments on their balance sheets, particularly with respect to middle and upper-middle-market sized issuers. Instead, many commercial banks have adopted an “underwrite-and-distribute” approach, which HPS believes is often less attractive to corporate borrowers seeking certainty of capital. As a result, commercial banks’ share of the leveraged loan market declined from approximately 71% in 1994 to approximately 14% in 20205. Access to the syndicated leveraged loan market has also become challenging for both first time issuers and smaller scale issuers, who previously had access to the capital markets. Issuers of tranche sizes representing less than $500 million account for just 9.5% of the new issue market as of December 31, 2020 as compared to over 45% in 20016. HPS believes that these regulatory actions have caused a shift in the role that commercial banks play in the direct lending market for middle to upper middle market borrowers, creating a void in the financing marketplace. This void has been filled by direct lending platforms which seek to provide borrowers an alternative “originate and retain” solution. In response, corporate borrower behavior has increasingly shifted to a more conscious assessment of the benefits that private capital from strategic financing partners can offer. |

• |

Volatility in Credit Markets has made Availability of Capital Less Predictable. HPS believes that the value of direct lending platforms for borrowers hinges on providing certainty of capital at a fair economic price. Volatility in the credit markets, coupled with changes to the regulatory framework over the past several years, has resulted in an imbalance between the availability of new loans to middle market borrowers and the demand from borrowers requiring capital for acquisitions, capital expenditures, recapitalizations, refinancings and restructurings. HPS believes that the scarcity of the supply of traditional loan capital relative to the demand has created an environment where direct lenders can often negotiate loans with attractive returns and creditor protections. |

• |

Increasingly Larger Borrowers Are Finding Value in Private Solutions. HPS believes the opportunity set has subtly shifted toward larger borrowers in recent times. The private credit focus on the middle market was traditionally driven by borrowers’ inefficient access to capital, and the fact that such borrowers were too small to have a syndicated loan or high yield bond. At the upper end of the middle market, companies have traditionally had the option to pursue a broadly syndicated loan, but recent volatility has increased the value they appear to be placing on the confidentiality, efficiency and execution certainty that is available in the private credit market. HPS believes that as borrowers and debt advisors become more aware of the depth in the private debt space that has been created by scaled providers, they will increasingly weigh this option against public market alternatives for larger companies. HPS believes the benefits of this growing opportunity set at the upper end of the market will accrue to the largest direct lending players, like HPS, as scale is a prerequisite for providing certainty. |

4 |

Source: Moody’s Investors Service Ultimate Recovery Rates Data; “Corporate Defaults and Recoveries - US” as of May 18, 2021. |

5 |

Source: S&P LCD Quarterly Leveraged Lending Review 4Q 2020, Primary Investor Market: Banks vs. Non-banks. |

6 |

Source: S&P LCD Middle Market Deal Size Category Factsheet 4Q 2020. |

Q: |

How will you identify investments? |

A: |

We believe that much of the value HPS will create for our private investment portfolio will come on the front end through the diversity of its sourcing capabilities. To source transactions, HPS will leverage the breadth of its global credit platform, and its shared knowledge and insights gleaned across both private and public credit, to cast a wide net to drive significant transaction flow. HPS will seek to generate investment opportunities across its various sourcing channels, including financial intermediaries such as investment banks and debt advisory firms, direct relationships with companies and management teams, private equity sponsors and formal partnerships and strategic arrangements with select financial institutions. We believe that this multi-pronged approach to sourcing will provide a significant pipeline of investment opportunities for us that could contribute to a portfolio for the Fund with attractive investment economics and risk/reward profiles.

|

Q: |

How will you evaluate and manage investments? |

A: |

HPS will evaluate and manage investments by adhering to the core principles of rigorous fundamental analysis, thorough due diligence, active portfolio monitoring and risk management.

|

• |

Rigorous Investment Screening and Selection. HPS expects the Fund to benefit from HPS’s global sourcing platforms and will seek to build a strong pipeline of investment opportunities. From this pipeline, certain investments proceed to an initial screening discussion that focuses on establishing the framework for the viability of the investment opportunity and the reasons to make the investment (i.e., leading market share, sustainable franchise and brand value, and value-add products or services). When evaluating a loan, the Fund’s investment team (the “Investment Team”) will focus on a combination of business stability, asset values and contractual loan protections. This process seeks to screen out companies that do not meet our risk criteria, while simultaneously prioritizing opportunities where the borrower may place greater emphasis on certain non-economic characteristics, such as certainty of scaled capital, creative financing solutions, an ability to understand complexity of capital structure or business risk and/or confidentiality of operating and financial performance. HPS believes that it has the greatest potential competitive edge over certain syndicated financing solutions or other competitive direct lending platforms to extract compelling risk-adjusted returns in these situations. |

• |

Fundamental Analysis and Due Diligence. The Investment Team’s approach to investment selection is anchored around conducting rigorous upfront, “private equity style” due diligence. The Investment Team’s due diligence and risk management processes will utilize and benefit from the substantial resources within HPS, as well as the Investment Team’s extensive relationships with management teams, industry experts, consultants, and outside advisors. In addition, the Investment Team employs a comprehensive investment process, which may include in-depth due diligence and full credit analysis on transaction drivers, investment thesis, review of business, industry and borrower risks and mitigants, competitive analysis, management calls/meetings, financial analysis of historical results, detailed financial forecasting, examination of legal structure/terms/collateral, relative value analysis, consulting with external experts and other considerations that the Investment Team deems appropriate. HPS generally seeks to employ a “cradle to grave” approach with respect to its investments such that the Investment Team is responsible for sourcing the investment, investment due diligence, and monitoring the investment until the investment is exited. HPS believes that this distinctive approach leads to greater connectivity between HPS and a borrower’s management teams, improved access to the borrower details and increased accountability, while simultaneously reducing the inherent risk of knowledge loss that exists where the sourcing, diligence and monitoring roles are bifurcated. |

• |

Structuring and Negotiating Downside Protection Mechanisms. From an investment process perspective, the Investment Team spends a significant amount of time and resources on structuring prior to committing to an investment, integrating both business-specific due diligence and risk findings into the overall structure and covenants of a particular transaction. The upfront structuring of these mechanisms, as well as the establishment of “early warning” information indicators, is critical to providing HPS with the tools needed to manage underperforming investments while seeking to preserve principal. This approach allows HPS to have early discussions, typically before a payment default, with |

• |

Disciplined Approach. The Investment Team expects to apply a highly selective, disciplined investment approach to the substantial transaction sourcing pipeline. As a result, the Investment Team expects to identify and invest in only a select number of attractive investment opportunities relative to the entire opportunity set. By adhering to the platform’s core principles of rigorous fundamental analysis, significant due diligence and active risk management, the Investment Team seeks to build an investment portfolio consisting primarily of senior secured loan investments that it believes will generate an attractive risk-adjusted return profile. |

Q: |

How will investments be allocated to the Fund? |

A: |

HPS provides investment management services to investment funds and client accounts. HPS will share any investment and sale opportunities with its other clients and the Fund in accordance with applicable law, including the Investment Advisers Act of 1940, as amended (the “Advisers Act”), firm-wide allocation policies, and an exemptive order from the SEC permitting co-investment activities (as further described below), which generally provide for sharing eligible investments pro rata among the eligible participating funds and accounts, subject to certain allocation factors.

|

Q: |

Will the Fund use leverage? |

A: |

Yes, we intend to use leverage to seek to enhance our returns. Our leverage levels will vary over time in response to general market conditions, the size and compositions of our investment portfolio and the views of our Adviser and Board. Once we have established a scaled and diversified investment portfolio, we expect that our debt to equity ratio will generally range between 1.0x and 1.5x. While our leverage employed may be greater or less than these levels from time to time, it will never exceed the limitations set forth in the 1940 Act, which currently allows us to borrow up to a 2:1 debt to equity ratio.

|

Q: |

What is a BDC? |

A: |

Congress created the business development company, or BDC, through the Small Business Investment Incentive Act of 1980 to facilitate capital investment in small and middle market companies. Closed-end investment companies organized in the U.S. that elect to be treated as BDCs under the 1940 Act are subject to specific provisions of the law, most notably that at least 70% of their total assets must be “qualifying assets”. Qualifying assets are generally defined as privately offered debt or equity securities of U.S. private companies or U.S. publicly traded companies with market capitalizations less than $250 million.

|

Q: |

What is a non-exchange traded, perpetual-life BDC? |

A: |

A non-exchange traded BDC’s shares are not listed for trading on a stock exchange or other securities market. The term “perpetual-life” is used to differentiate our structure from other BDCs who have a finite offering period and/or have a predefined time period to pursue a liquidity event or to wind down the fund. In contrast, in a perpetual-life BDC structure like ours, we expect to offer common shares continuously at a price equal the monthly net asset value (“NAV”) per share and we have an indefinite duration, with no obligation to effect a liquidity event at any time. We generally intend to offer our common shareholders an opportunity to have their shares repurchased on a quarterly basis, subject to an aggregate cap of 5% of shares outstanding. However, the determination to repurchase shares in any given quarter is fully at the Board’s discretion, so investors may not always have access to liquidity when they desire it. See “Risk Factors.”

|

Q: |

How will an investment in HLEND differ from an investment in a listed BDC or private BDC with a finite life? |

A: |

An investment in our common shares of beneficial interest (“Common Shares”) differs from an investment in a listed or exchange traded BDC in several ways, including:

|

• |

Pricing. Following our initial public offering, the value at which our new Common Shares may be offered, or our Common Shares may be repurchased, will be equal to our monthly NAV per share. In contrast, shares of listed BDCs are priced by the trading market, which can be influenced by a variety of factors, including many that are not directly related to the underlying value of an entity’s assets and liabilities. The prices of listed BDCs are often higher or lower than the fund’s NAV per share and can be subject to volatility, particularly during periods of market stress. |

• |

Liquidity. An investment in our Common Shares has limited or no liquidity beyond our share repurchase program, and our share repurchase program can be modified, suspended or terminated at the Board’s discretion. In contrast, a listed BDC is a liquid investment, as shares can be sold on the exchange at any time the exchange is open. |

• |

Oversight. Both listed BDCs and non-traded BDCs are subject to the requirements of the 1940 Act and the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Unlike the offering of a listed BDC, the Fund’s offering will be registered in every state in which we are offering and selling shares. As a result, we include certain limits in our governing documents that are not typically provided for in the charter of a listed BDC. For example, out charter limits the fees we can pay to the Adviser. |

• |

Eligible Investors. Our Common Shares may be purchased by any investor who meets the minimum suitability requirements described under “Suitability Standards” in this prospectus. While the standard |

• |

Investment funding. Purchases of our Common Shares must be fully funded at the time of subscription. In contrast, investors typically make an upfront commitment in the context of a privately placed BDC and their capital is subsequently called over time as investments are made. |

• |

Investment period. We have a perpetual life and may continue to take in new capital on a continuous basis at a value generally equal to our NAV per share. We will be continually originating new investments to the extent we raise additional capital. We will also be regularly recycling capital from our existing investors into new investments. In contrast, privately placed BDCs generally have a finite offering period and an associated designated time period for investment. In addition, many privately placed BDCs have either a finite life or time period by which a liquidity event must occur or fund operations must be wound down, which may limit the ability of the fund to recycle investments. |

Q: |

For whom may an investment in the Fund be appropriate? |

A: |

An investment in our shares may be appropriate for you if you: |

• |

meet the minimum suitability requirements described under “Suitability Standards” above, which generally require that a potential investor has either (i) both net worth and annual net income of $70,000 or (ii) net worth of at least $250,000; |

• |

seek to allocate a portion of your financial assets to a direct investment vehicle with an income-oriented portfolio of primarily U.S. credit investments; |

• |

seek to receive current income through regular distribution payments while obtaining the potential benefit of long-term capital appreciation; and |

• |

can hold your shares as a long-term investment without the need for near-term or rapid liquidity. |

Q: |

Will HPS be investing in the Fund? |

A: |

Yes, an affiliate of HPS plans to invest up to $25 million in our Common Shares through one or more private placement transactions. In addition, officers and employees of HPS and its affiliates may also purchase our Common Shares. Purchases made by HPS, its affiliates and their respective officers and directors will not count towards satisfaction of our minimum offering amount.

|

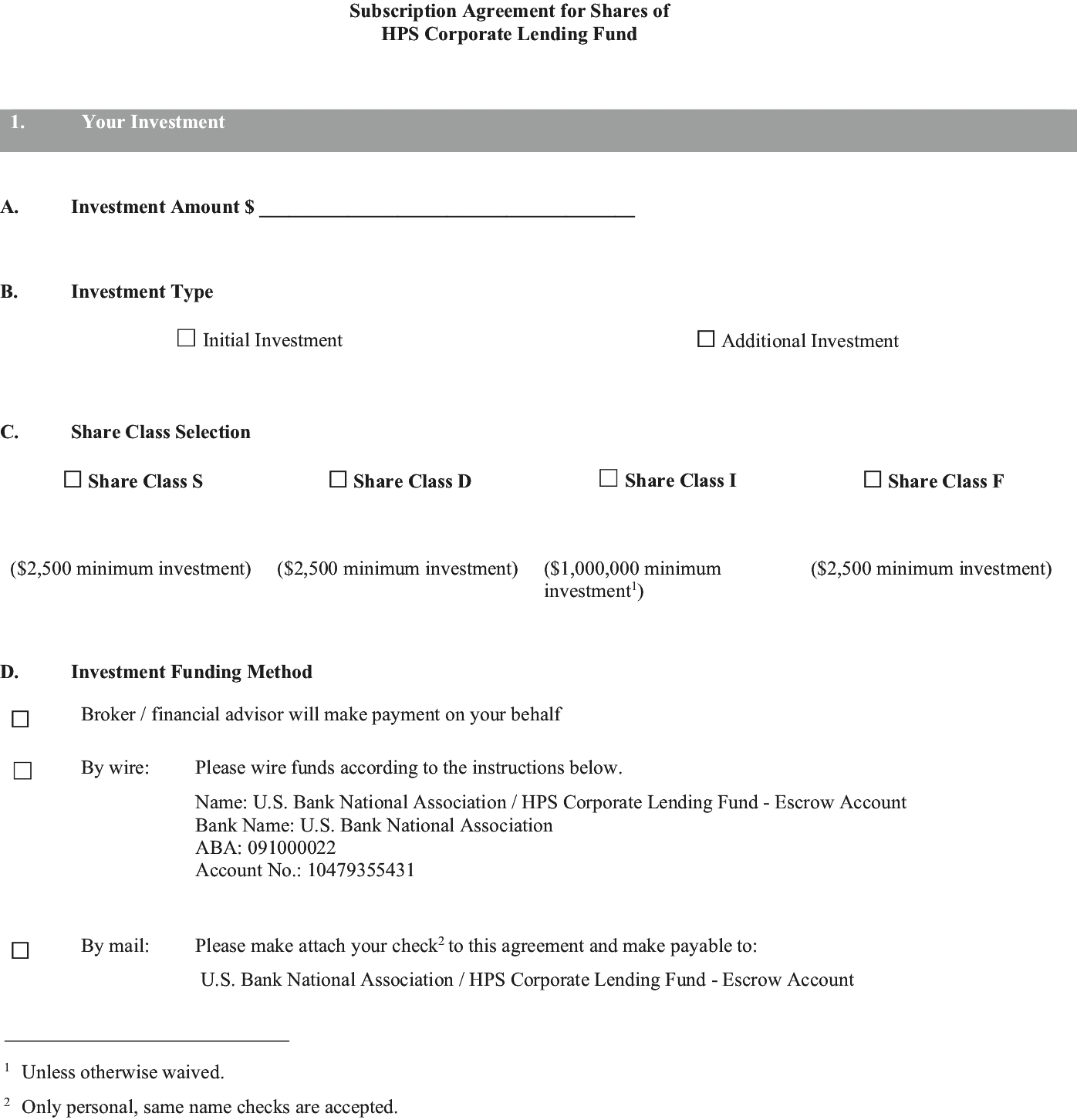

Q: |

Is there any minimum investment required? |

A: |

Yes, to purchase Class S, Class D or Class F shares in this offering, you must make a minimum initial investment in our Common Shares of $2,500. To purchase Class I shares in this offering, you must make a minimum initial investment of $1,000,000. All subsequent purchases of Class S, Class D, Class F or Class I shares, except for those made under our distribution reinvestment plan, are subject to a minimum investment size of $500 per transaction. The Managing Dealer can waive the initial or subsequent minimum investment at its discretion.

|

Q: |

How will the Fund’s value be established? |

A: |

Immediately upon the conclusion of the escrow period, the Fund’s NAV will be equal to the net proceeds received by us from purchases of Common Shares during the escrow period, less our liabilities. Thereafter, our NAV will be determined based on the value of our assets less our liabilities, including accrued fees and expenses, as of any date of determination.

|

Q: |

How can I purchase shares? |

A: |

Subscriptions to purchase our Common Shares may be made on an ongoing basis, but after the time that we break escrow for this offering, investors may only purchase our Common Shares pursuant to accepted subscription orders as of the first business day of each month. A subscription must be received in good order at least five business days prior to the first business day of the month (unless waived by the Managing Dealer) and include the full subscription funding amount to be accepted.

|

Q: |

When will my subscription be accepted? |

A: |

Completed subscription requests will not be accepted by us any earlier than two business days before the first day of each month.

|

Q: |

Can I withdraw a subscription to purchase shares once I have made it? |

A: |

Yes, you may withdraw a subscription after submission at any time before we have accepted the subscription, which we will generally not do any earlier than two business days before the first day of each month. You may withdraw your purchase request by notifying the transfer agent, through your financial intermediary or directly on the toll-free, automated telephone line at 1-888-484-1944.

|

Q: |

What is the per share purchase price? |

A: |

During the escrow period, the per share purchase price for our Common Shares will be $25.00. After the close of the escrow period, shares will be sold at the then-current NAV per share, as described above.

|

Q: |

When will the NAV per share be available after the escrow period? |

A: |

We will report our NAV per share as of the last day of each month on our website within 20 business days of the last day of each month. Because subscriptions must be submitted at least five business days prior to the first day of each month, you will not know the NAV per share at which you will be subscribing at the time you subscribe.

|

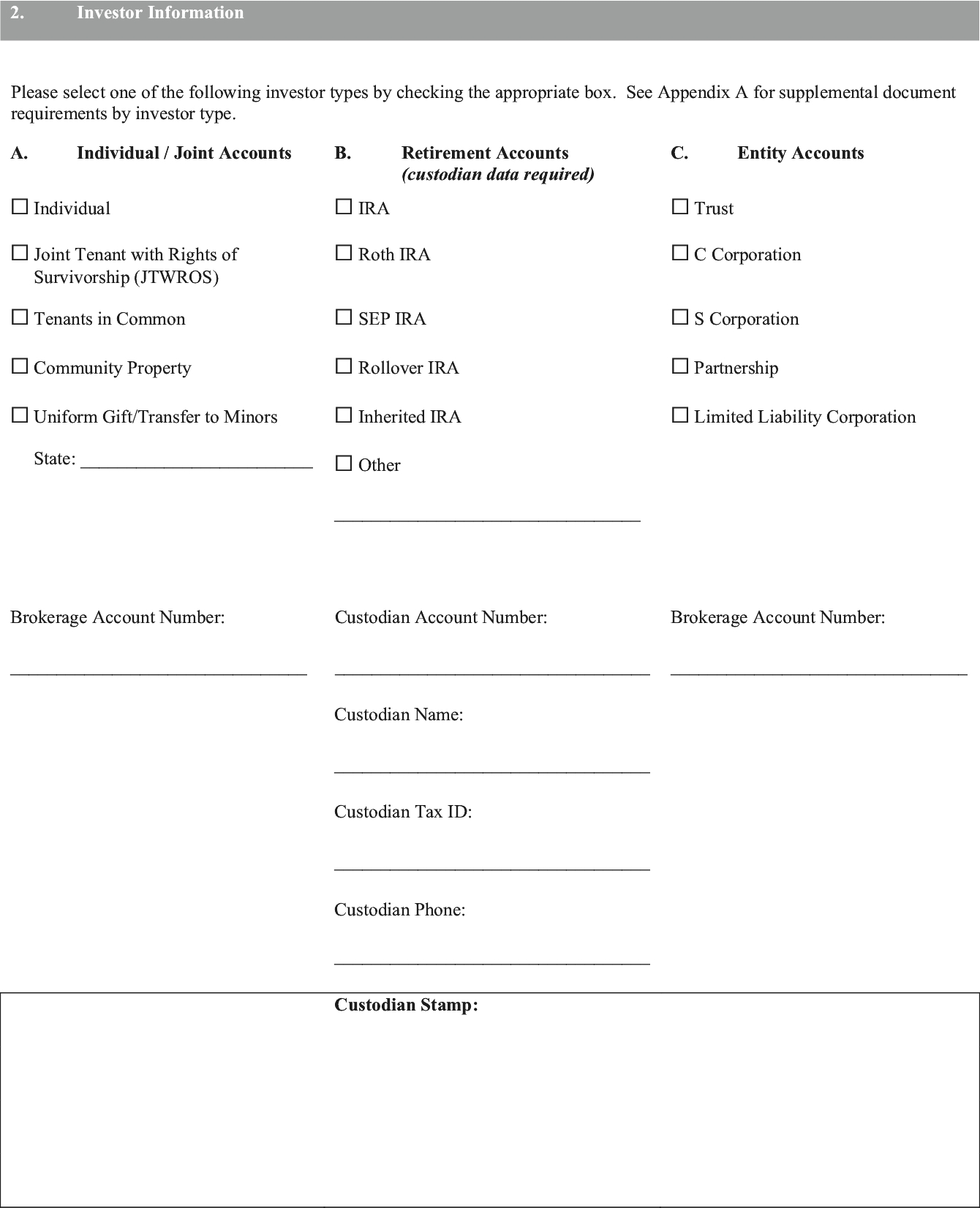

Q: |

Can I invest through my Individual Retirement Account (“IRA”), Simplified Employee Pension Plan (“SEP”) or other after-tax deferred account? |

A: |

Yes, if you meet the suitability standards described under “Suitability Standards” above, you may invest via an IRA, SEP or other after-tax deferred account. If you would like to invest through one of these account types, you should contact your custodian, trustee or other authorized person for the account to subscribe. They will process the subscription and forward it to us, and we will send the confirmation and notice of our acceptance back to them.

|

Q: |

How often will the Fund pay distributions? |

A: |

We expect to pay regular monthly distributions commencing with the first full calendar quarter after the escrow period concludes. Any distributions we make will be at the discretion of our Board, who will consider, among other things, our earnings, cash flow, capital needs and general financial condition, as well as our desire to comply with the RIC requirements, which generally require us to make aggregate annual distributions to our shareholders of at least 90% of our net investment income. As a result, our distribution rates and payment frequency may vary from time to time and there is no assurance we will pay distributions in any particular amount, if at all. See “Description of our Common Shares” and “Certain U.S. Federal Income Tax Considerations.”

|

Q: |

Can I reinvest distributions in the Fund? |

A: |

Yes, we have adopted a distribution reinvestment plan whereby shareholders (other than those located in specific states or who are clients of selected participating brokers, as outlined below) will have their cash distributions automatically reinvested in additional shares of the same class of our Common Shares to which the distribution relates unless they elect to receive their distributions in cash. The purchase price for shares purchased under our distribution reinvestment plan will be equal to the then current NAV per share of the relevant class of Common Shares. Shareholders will not pay transaction related charges when purchasing shares under our distribution reinvestment plan, but all outstanding Class S, Class D and Class F shares, including those purchased under our distribution reinvestment plan, will be subject to ongoing servicing fees.

|

Q: |

How can I change my distribution reinvestment plan election? |

A: |

Participants may terminate their participation in the distribution reinvestment plan or shareholders may elect to participate in our distribution reinvestment plan with five business days’ prior written notice by contacting our Transfer Agent, U.S. Bancorp Fund Services, LLC (d/b/a U.S. Bank Global Fund Services) (“U.S. Bank Global Fund Services”), at HPS Corporate Lending Fund, c/o U.S. Bank Global Fund Services, 615 East Michigan Street, Milwaukee, WI 53202.

|

Q: |

How will distributions be taxed? |

A: |

We intend to elect to be treated for federal income tax purposes, and intend to qualify annually thereafter, as a RIC under the Code. A RIC is generally not subject to U.S. federal corporate income taxes on the net taxable income that it currently distributes to its shareholders.

|

Q: |

Can I sell, transfer or otherwise liquidate my shares post purchase? |

A: |

The purchase of our Common Shares is intended to be a long-term investment. We do not intend to list our shares on a national securities exchange, and do not expect a public market to develop for our shares in the foreseeable future. We also do not intend to complete a liquidity event within any specific period, and there can be no assurance that we will ever complete a liquidity event. We do intend to conduct quarterly share repurchase offers in accordance with the 1940 Act to provide limited liquidity to our shareholders. Our share repurchase program will be the only liquidity initiative that we offer to our shareholders.

|

Q: |

Can I request that my shares be repurchased? |

A: |

Yes, you can request that your shares be repurchased subject to the following limitations. Beginning no later than the first full calendar quarter from the date on which we break escrow for this offering, and subject to the discretion of the Board, we intend to commence a share repurchase program pursuant to which we

|

Q: |

What fees do you pay to the Adviser? |

A: |

Pursuant to the advisory agreement between us and the Adviser (the “Advisory Agreement”), the Adviser is responsible for, among other things, identifying investment opportunities, monitoring our investments and determining the composition of our portfolio. We will pay the Adviser a fee for its services under the Advisory Agreement consisting of two components: a management fee and an incentive fee.

|

• |

The management fee is payable monthly in arrears at an annual rate of 1.25% of the value of our net assets as of the beginning of the first calendar day of the applicable month. For the first calendar month in which the Fund has operations, net assets will be measured as the beginning net assets as of the date on which the Fund breaks escrow. In addition, the Adviser has agreed to waive its management fee for the first six months following the date on which we break escrow for this offering. The longer an investor holds our Common Shares during this period, the longer such investor will receive the benefit of this management fee waiver. |

• |

The incentive fee will consist of two components as follows: |

• |

The first part of the incentive fee is based on income, whereby we will pay the Adviser quarterly in arrears 12.5% of its Pre-Incentive Fee Net Investment Income Returns (as defined below), attributable to each class of the Fund’s Common Shares, for each calendar quarter subject to a 5.0% annualized hurdle rate, with a catch-up. The Adviser has agreed to waive the incentive fee based on income for the first six months following the date on which we break escrow for this offering. The longer an investor holds our Common Shares during this period, the longer such investor will receive the benefit of this income based incentive fee waiver. |

• |

The second part of the incentive fee is based on realized capital gains, whereby we will pay the Adviser at the end of each calendar year in arrears 12.5% of cumulative realized capital gains, attributable to each class of the Fund’s Common Shares, from inception through the end of such calendar year, computed net of all realized capital losses and unrealized capital depreciation on a cumulative basis, less the aggregate amount of any previously paid incentive fee on capital gains. |

Q: |

How will I be kept up to date about how my investment is doing? |

A: |

We and/or your financial advisor, participating broker or financial intermediary, as applicable, will provide you with periodic updates on the performance of your investment with us, including:

|

• |

three quarterly financial reports and an annual report; |

• |

quarterly investor statements; |

• |

in the case of certain U.S. shareholders, an annual Internal Revenue Service (“IRS”) Form 1099-DIV or IRS Form 1099-B, if required, and, in the case of non-U.S. shareholders, an annual IRS Form 1042-S; and |

• |

confirmation statements (after transactions affecting your balance, except reinvestment of distributions in us and certain transactions through minimum account investment or withdrawal programs). |

Q: |

What type of tax reporting will I receive on the Fund, and when will I receive it? |

A: |

As promptly as possible after the end of each calendar year, we intend to send to each of our U.S. shareholders an annual IRS Form 1099-DIV or IRS Form 1099-B, if required, and, in the case of non-U.S. shareholders, an annual IRS Form 1042-S.

|

Q: |

What are the tax implications for non-U.S. investors in the Fund? |

A: |

Because we are a corporation for U.S. federal income tax purposes, a non-U.S. investor in the Fund will generally not be treated as engaged in a trade or business in the U.S. solely as a result of investing in the Fund, unless the Fund is treated as a “United States real property holding corporation” for U.S. federal income tax purposes. Although there can be no assurance in this regard, we do not currently expect to be a United States real property holding corporation for U.S. federal income tax purposes.

|

Q: |

What are the tax implications for non-taxable U.S. investors in the Fund? |

A: |

Because we are a corporation for U.S. federal income tax purposes, U.S. tax-exempt investors in the Fund will generally not derive “unrelated business taxable income” for U.S. federal income tax purposes (“UBTI”) solely as a result of their investment in the Fund. A U.S. tax-exempt investor, however, may derive UBTI from its investment in the Fund if the investor incurs indebtedness in connection with its purchase of shares in the Fund. Tax-exempt investors should consult their tax advisors with respect to the consequences of investing in the Fund.

|

Q: |

What is the difference between the four classes of Common Shares being offered? |

A: |

We are offering to the public four classes of Common Shares - Class S shares, Class D shares, Class I shares and Class F shares. The differences among the share classes relate to ongoing shareholder servicing and/or distribution fees, with Class S shares, Class D shares and Class F shares subject to ongoing and shareholder servicing and/or distribution fee of 0.85%, 0.25% and 0.50%, respectively and Class I shares not subject to a shareholder servicing and/or distribution fee. In addition, although no upfront sales loads will be paid with respect to Class S shares, Class D shares, Class I shares or Class F shares, if you buy Class S shares, Class D shares or Class F shares through certain financial intermediaries, they may directly charge you transaction or other fees, including upfront placement fees or brokerage commissions, in such amount as they may determine, provided that they limit such charges to a 3.5% cap on NAV for Class S shares, a 2.0% cap on NAV for Class D shares and a 2.0% cap on NAV for Class F shares. Selling agents will not charge such fees on Class I shares. See “Description of Our Common Shares” and “Plan of Distribution” in our N-2 registration statement for a discussion of the differences between our Class S, Class D, Class I and Class F shares. See “Description of Our Common Shares” and “Plan of Distribution” for a discussion of the differences between our Class S, Class D, Class I and Class F shares.

|

| | |

Annual Shareholder

Servicing and/or

Distribution Fees

|

| |

Total Over

Five Years

|

|

Class S

|

| | $85 |

| | $425 |

Class D

|

| | $25 |

| | $125 |

Class I

|

| | $0

|

| | $0

|

Class F

|

| | $50 |

| | $250 |

Q: |

Are there ERISA considerations in connection with investing in the Fund? |

A: |

We intend to conduct our affairs so that our assets should not be deemed to constitute “plan assets” under the ERISA, and certain U.S. Department of Labor regulations promulgated thereunder, as modified by Section 3(42) of ERISA (the “Plan Asset Regulations”). In this regard, until such time as all classes of the

|

Q: |

What is the role of the Fund’s Board of Trustees? |

A: |

We operate under the direction of our Board, the members of which are accountable to us and our shareholders as fiduciaries. We have five Trustees, three of whom have been determined to be independent of us, the Adviser and its affiliates (“Independent Trustees”). Our Independent Trustees are responsible for, among other things, reviewing the performance of the Adviser, approving the compensation paid to the Adviser and its affiliates, oversight of the valuation process used to establish the Fund’s NAV and oversight of the investment allocation process to the Fund. The names and biographical information of our Trustees are provided under “Management of the Fund—Trustees and Executive Officers.”

|

Q: |

Are there any risks involved in buying your shares? |

A: |

Investing in our Common Shares involves a high degree of risk. If we are unable to effectively manage the impact of these risks, we may not meet our investment objective and, therefore, you should purchase our shares only if you can afford a complete loss of your investment. An investment in our Common Shares involves significant risks and is intended only for investors with a long-term investment horizon and who do not require immediate liquidity or guaranteed income. Some of the more significant risks relating to an investment in our Common Shares include those listed below:

|

• |

We have no prior operating history and there is no assurance that we will achieve our investment objective. |

• |

This is a “blind pool” offering and thus you will not have the opportunity to evaluate our investments before we make them. |

• |

You should not expect to be able to sell your shares regardless of how we perform. |

• |

You should consider that you may not have access to the money you invest for an extended period of time. |

• |

We do not intend to list our shares on any securities exchange, and we do not expect a secondary market in our shares to develop prior to any listing. |

• |

Because you may be unable to sell your shares, you will be unable to reduce your exposure in any market downturn. |

• |

We intend to implement a share repurchase program, but only a limited number of shares will be eligible for repurchase and repurchases will be subject to available liquidity and other significant restrictions. |

• |

An investment in our Common Shares is not suitable for you if you need access to the money you invest. See “Suitability Standards” and “Share Repurchase Program.” |

• |

We cannot guarantee that we will make distributions, and if we do we may fund such distributions from sources other than cash flow from operations, including, without limitation, the sale of assets, borrowings, or return of capital, and we have no limits on the amounts we may pay from such sources. |

• |

Distributions may also be funded in significant part, directly or indirectly, from temporary waivers or expense reimbursements borne by the Adviser or its affiliates, that may be subject to reimbursement to the Adviser or its affiliates. The repayment of any amounts owed to the Advisor or its affiliates will reduce future distributions to which you would otherwise be entitled. |

• |

We expect to use leverage, which will magnify the potential for loss on amounts invested in us. |

• |

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”), and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies will make our Common Shares less attractive to investors. |

• |

We intend to invest primarily in securities that are rated below investment grade by rating agencies or that would be rated below investment grade if they were rated. Below investment grade securities, which are often referred to as “junk,” have predominantly speculative characteristics with respect to the issuer’s capacity to pay interest and repay principal. They may also be illiquid and difficult to value. |

Q: |

Do you currently own any investments? |

A: |

No. |

Q: |

At what point will the initial proceeds of this offering be released from escrow? |

A: |

We will take purchase orders and hold investors’ funds in an interest-bearing escrow account until we receive purchase orders for at least $100 million (excluding any shares purchased by our Adviser, its affiliates and our Trustees and officers but including any shares purchased in any private offerings), and our Board has authorized the release of the escrowed purchase order proceeds to us so that we can commence operations. Even if we receive purchase orders for $100 million, our Board may elect to wait a substantial amount of time before authorizing, or may elect not to authorize, the release of the escrowed proceeds. If we do not raise the minimum amount and commence operations by [ ], 2022 (one year following the effective date of the registration statement of which this prospectus is a part), this offering will be terminated and our escrow agent will promptly send you a full refund of your investment with interest and without deduction for escrow expenses. Notwithstanding the foregoing, you may elect to withdraw your purchase order and request a full refund of your investment with interest and without deduction for escrow expenses at any time before the escrowed funds are released to us. If we break escrow for this offering and commence operations, interest earned on funds in escrow will be released to our account and constitute part of our net assets.

|

Q: |

What is a “best efforts” offering? |

A: |

This is our initial public offering of our Common Shares on a “best efforts” basis. A “best efforts” offering means the Managing Dealer and the participating brokers are only required to use their best efforts to sell the shares. When shares are offered to the public on a “best efforts” basis, no underwriter, broker or other person has a firm commitment or obligation to purchase any of the shares. Therefore, we cannot guarantee that any minimum number of shares will be sold.

|

Q: |

What is the expected term of this offering? |

A: |

We have registered $2,000,000,000 in Common Shares. It is our intent, however, to conduct a continuous offering for an extended period of time, by filing for additional offerings of our shares, subject to regulatory approval and continued compliance with the rules and regulations of the SEC and applicable state laws.

|

Q: |

What is a regulated investment company, or RIC? |

A: |

We intend to elect to be treated for federal income tax purposes, and intend to qualify annually thereafter, as a regulated investment company (a “RIC”) under the Internal Revenue Code of 1986, as amended (the “Code”).

|

• |

is a BDC or registered investment company that combines the capital of many investors to acquire securities; |

• |

offers the benefits of a securities portfolio under professional management; |

• |

satisfies various requirements of the Code, including an asset diversification requirement; and |

• |

is generally not subject to U.S. federal corporate income taxes on its net taxable income that it currently distributes to its shareholders, which substantially eliminates the “double taxation” (i.e., taxation at both the corporate and shareholder levels) that generally results from investments in a C corporation. |

Q: |

Who will administer the Fund? |

A: |

HPS, in its capacity as our administrator (the “Administrator”), will provide, or oversee the performance of, administrative and compliance services. We will reimburse the Administrator for its costs, expenses and the Fund’s allocable portion of compensation of the Administrator’s personnel and the Administrator’s overhead (including rent, office equipment and utilities) and other expenses incurred by the Administrator in performing its administrative obligations under the administration agreement (the “Administration Agreement”). See “Advisory Agreement and Administration Agreement—Administration Agreement.”

|

Q: |

What are the offering and servicing costs? |

A: |

No upfront sales load will be paid with respect to Class S shares, Class D shares, Class I or Class F shares; however, if you buy Class S shares, Class D shares or Class F shares through certain financial intermediaries, they may directly charge you transaction or other fees, including upfront placement fees or brokerage commissions, in such amount as they may determine, provided that they limit such charges to a 3.5% cap on NAV for Class S shares, a 2.0% cap on NAV for Class D shares and a 2.0% cap on NAV for Class F shares. Selling agents will not charge such fees on Class I shares. Please consult your selling agent for additional information.

|

Q: |

What are our expected operating expenses? |

A: |

We expect to incur operating expenses in the form of our management and incentive fees, shareholder servicing and/or distribution fees, interest expense on our borrowings and other expenses, including the fees we pay to our Administrator. See “Fees and Expenses.”

|

Q: |

What are our policies related to conflicts of interests with HPS and its affiliates? |

A: |

The Adviser and its affiliates will be subject to certain conflicts of interest with respect to the services HPS (in its capacity as the Adviser and the Administrator) provide for us. These conflicts will arise primarily from the involvement of HPS in other activities that may conflict with our activities. You should be aware that individual conflicts will not necessarily be resolved in favor of our interest.

|

• |

Conflicts of Interest Generally. In the ordinary course of its business activities, HPS will engage in activities where the interests of certain of its own interests or the interests of its clients will conflict with the interests of the shareholders in the Fund. Other present and future activities of the Firm will give rise to additional conflicts of interest. In the event that a conflict of interest arises, the Adviser will attempt to resolve such conflict in a fair and equitable manner. Subject to applicable law, including the 1940 Act, and the Board of Trustees’ oversight, the Adviser will have the power to resolve, or consent to the resolution of, conflicts of interest on behalf of the Fund. Investors should be aware that conflicts will not necessarily be resolved in favor of the Fund’s interests. In addition, the Adviser may in certain situations choose to consult with or obtain the consent of the Board of Trustees with respect to any specific conflict of interest, including with respect to the approvals required under the 1940 Act, including Section 57(f), and the Advisers Act. The Fund may enter into joint transactions or cross-trades with clients or affiliates of the Adviser to the extent permitted by the 1940 Act, the Advisers Act and any applicable co-investment order from the SEC. Subject to the limitations of the 1940 Act, the Fund may invest in loans or other securities, the proceeds of which may refinance or otherwise repay debt or securities of companies whose debt is owned by other HPS funds and accounts. |

• |

Relationship among the Fund, the Adviser and the Investment Team. The Adviser has a conflict of interest between its responsibility to act in the best interests of the Fund, on the one hand, and any benefit, monetary or otherwise, that results to it or its affiliates from the operation of the Fund, on the other hand. For example, the incentive fee creates an incentive for the Adviser to recommend more speculative investments for the Fund than it would otherwise in the absence of such performance-based compensation. |

• |

Co-Investment Transactions. The Fund has applied for an exemptive order from the SEC that permits it to co-invest with certain other persons, including certain affiliated accounts managed and controlled by the Adviser. Subject to the 1940 Act and the conditions of any such co-investment order issued by the SEC, the Fund may, under certain circumstances, co-invest with certain affiliated accounts in investments that are suitable for the Fund and one or more of such affiliated accounts. Even though the Fund and any such affiliated account co-invest in the same securities, conflicts of interest may still arise. If the Adviser is presented with co-investment opportunities that generally fall within the Fund’s investment objective and other Board-established criteria and those of one or more affiliated accounts advised by the Adviser, whether focused on a debt strategy or otherwise, the Adviser will allocate such opportunities among the Fund and such affiliated accounts in a manner consistent with the exemptive order and the Adviser’s allocation policies and procedures. There is no assurance that the co-investment exemptive order will be granted by the SEC. |

• |

Competition among the Accounts Managed by the Adviser and Its Affiliates. The Affiliated Group is actively engaged in advisory and management services for multiple collective investment vehicles and managed accounts (each, an “Affiliated Group Account” and together, the “Affiliated Group Accounts”). The Affiliated Group expects to sponsor or manage additional collective investment vehicles and managed accounts in the future. The Affiliated Group may employ the same or different investment strategies for the various Affiliated Group Accounts it manages or otherwise advises. |

Q: |

What is the impact of being an “emerging growth company”? |

A: |

We are an “emerging growth company,” as defined by the JOBS Act. As an emerging growth company, we are eligible to take advantage of certain exemptions from various reporting and disclosure requirements that are applicable to public companies that are not emerging growth companies. For so long as we remain an emerging growth company, we will not be required to:

|

• |

have an auditor attestation report on our internal control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002 (“Sarbanes-Oxley Act”); |

• |

submit certain executive compensation matters to shareholder advisory votes pursuant to the “say on frequency” and “say on pay” provisions (requiring a non-binding shareholder vote to approve compensation of certain executive officers) and the “say on golden parachute” provisions (requiring a non-binding shareholder vote to approve golden parachute arrangements for certain executive officers in connection with mergers and certain other business combinations) of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010; or |

• |

disclose certain executive compensation related items, such as the correlation between executive compensation and performance and comparisons of the chief executive officer’s compensation to median employee compensation. |

Q: |

Who can help answer my questions? |

A: |

If you have more questions about this offering or if you would like additional copies of this prospectus, you should contact your financial advisor or our transfer agent at HPS Corporate Lending Fund, c/o U.S. Bank Global Fund Services, 615 East Michigan Street Milwaukee, WI 53202, or at 1-888-484-1944.

|

| | |

Class S

Shares

|

| |

Class D

Shares

|

| |

Class I

Shares

|

| |

Class F

Shares

|

|

Shareholder transaction expense (fees paid directly from your investment) |

| | | | | | | | ||||

Maximum sales load(1)

|

| |

—% |

| |

—% |

| |

—% |

| |

—% |

Maximum Early Repurchase Deduction(2)

|

| |

2.0% |

| |

2.0% |

| |

2.0% |

| | 2.0% |

| | | | | | | | | |||||

Annual expenses (as a percentage of net assets attributable to our Common Shares)(3) |

| | | | | | | | ||||

Base management fees(4)

|

| |

1.25% |

| |

1.25% |

| |

1.25% |

| | 1.25% |

Incentive fees(5)

|

| |

—% |

| |

—% |

| |

—% |

| |

—% |

Shareholder servicing and/or distribution fees(6)

|

| |

0.85% |

| |

0.25% |

| |

—% |

| |

0.50% |

Interest payment on borrowed funds(7)

|

| |

3.25% |

| |

3.25% |

| |

3.25% |

| |

3.25% |

Other expenses(8)

|

| |

1.30% |

| |

1.30% |

| |

1.30% |

| |

1.30% |

Total annual expenses

|

| |

6.65% |

| |

6.05% |

| |

5.80% |

| |

6.30% |

Expense Support(8)

|

| | (0.30)% |

| | (0.30)% |

| | (0.30)% |

| | (0.30)% |

Total annual expenses (after expense support)(8)

|

| | 6.35% |

| | 5.75% |

| | 5.50% |

| | 6.00% |

(1) |

No upfront sales load will be paid with respect to Class S shares, Class D shares, Class I shares or Class F shares; however, if you buy Class S shares, Class D shares or Class F shares through certain financial intermediaries, they may directly charge you transaction or other fees, including upfront placement fees or brokerage commissions, in such amount as they may determine, provided that they limit such charges to a 3.5% cap on NAV for Class S shares, a 2.0% cap on NAV for Class D shares and a 2.0% cap on NAV for Class F shares. Please consult your selling agent for additional information. |

(2) |

Under our share repurchase program, to the extent we offer to repurchase shares in any particular quarter, we expect to repurchase shares pursuant to tender offers using a purchase price equal to the NAV per share as of the last calendar day of the applicable quarter, except that shares that have not been outstanding for at least one year may be subject to a fee of 2.0% of such NAV. The one-year holding period is measured as of the subscription closing date immediately following the prospective repurchase date. The Early Repurchase Deduction may be waived in the case of repurchase requests arising from the death, divorce or qualified disability of the holder. The Early Repurchase Deduction will be retained by the Fund for the benefit of remaining shareholders. |

(3) |

Weighted average net assets employed as the denominator for expense ratio computation is $902 million. This estimate is based on the assumption that we sell $1,500,000,000 of our Common Shares in the initial 12-month period of the offering. Actual net assets will depend on the number of shares we actually sell, realized gains/losses, unrealized appreciation/ depreciation and share repurchase activity, if any. |

(4) |

The base management fee paid to our Adviser is calculated at an annual rate of 1.25% of the value of our net assets as of the beginning of the first calendar day of the applicable month. |

(5) |

We may have capital gains and investment income that could result in the payment of an incentive fee in the first year of investment operations. The incentive fees, if any, are divided into two parts: |

• |

The first part of the incentive fee is based on income, whereby we will pay the Adviser quarterly in arrears 12.5% of our Pre-Incentive Fee Net Investment Income Returns (as defined below), attributable to each class of the Fund’s Common Shares, for each calendar quarter subject to a 5.0% annualized hurdle rate, with a catch-up. |

• |

The second part of the incentive is based on realized capital gains, whereby we will pay the Adviser at the end of each calendar year in arrears 12.5% of cumulative realized capital gains, attributable to each class of the Fund’s Common Shares, from inception through the end of such calendar year, computed net of all realized capital losses and unrealized capital depreciation on a cumulative basis, less the aggregate amount of any previously paid incentive fee on capital gains. |

(6) |

Subject to FINRA limitations on underwriting compensation, we will also pay the following shareholder servicing and/or distribution fees to the Managing Dealer and/or a participating broker: (a) for Class S shares, a shareholder servicing and/or distribution fee equal to 0.85% per annum of the aggregate NAV as of the beginning of the first calendar day of the month for the Class S shares, (b) for Class D shares, a shareholder servicing fee equal to 0.25% per annum of the aggregate NAV as of the beginning of the first calendar day of the month for the Class D shares, and (c) for Class F shares, a shareholder servicing and/or distribution fee equal to 0.50% per annum of the aggregate NAV as of the beginning of the first calendar day of the month for the Class F shares, in each case, payable monthly. No shareholder servicing fees |

(7) |

We may borrow funds to make investments, including before we have fully invested the proceeds of this continuous offering. To the extent that we determine it is appropriate to borrow funds to make investments, the costs associated with such borrowing will be indirectly borne by shareholders. The figure in the table assumes that we borrow for investment purposes an amount equal to 100% of our weighted average net assets in the initial 12-month period of the offering, and that the average annual cost of borrowings, including the amortization of cost associated with obtaining borrowings and unused commitment fees, on the amount borrowed is 3.25%. Our ability to incur leverage during the 12 months following the commencement of this offering depends, in large part, on whether we meet our minimum offering requirement, the amount of money we are able to raise through the sale of shares registered in this offering and the availability of financing in the market. |

(8) |

“Other expenses” include accounting, legal and auditing fees, custodian and transfer agent fees, reimbursement of expenses to our Administrator, organization and offering expenses, insurance costs and fees payable to our Trustees, as discussed in “Plan of Operation.” The amount presented in the table estimates the amounts we expect to pay during the initial 12-month period of the offering prior to any expense support, as described below. |

| | | 1 Year |

| | 3 Years |

| | 5 Years |

| | 10 Years |

|