EX-99.1

Published on February 24, 2026

Exhibit 99.1

HPS Corporate Lending Fund HLEND: Software Q&A Q: How does HPS interpret the recent software headlines and broader market pessimism towards software investments? A : What’s happening in public software equities is a valuation reset following several years of multiple expansion . The software sector remains fundamentally important to enterprise and consumer workflows, but its market value is increasingly being reassessed as artificial intelligence reshapes product value, pricing power, and long-term growth expectations . Recent equity performance and valuation compression reflect both real disruption risks and heightened investor uncertainty around long-term sustainable growth rates, which have been the primary factor in software valuation . Q: What are the implications of the software revaluation for private credit? A : The software sector is a meaningful borrower group, so private credit implications are naturally part of the conversation . However, we don’t equate equity market selloffs with fundamental credit risk because the return paradigms and structure between equity and debt are completely different. While equity valuations and returns are driven by long -term growth outlook and terminal value expectations, private credit returns depend on cash flow generation for coupon and principal repayment over a shorter, contractually defined time frame. First lien private credit investments have typically been structured with 30 %—45 % loan-to-value ratios, with software -related loans often at the more conservative end of that range . We believe this provides significant protective cushion even if equity valuations are reduced . Furthermore, first lien senior private credit loans tend to have relatively short effective durations (typically 3 to 4 years ), and are typically generating average all-in yields in the 8% – 9%1 range . Q: What do you expect AI’s impact on software to be? A : We have been underwriting software companies with AI disruption in mind for some time. AI is reshaping the software landscape but not in a uniform or indiscriminate way . The software sector is not monolithic, and we do a company -by-company assessment to evaluate their resilience to competition and revenue stickiness . We have been focused on understanding where we believe AI enhances durable value versus where it erodes it. In our view, enterprise software providers that offer mission critical platforms, proprietary data and/or are embedded in workflows, and have strong customer relationships have been most resilient and may ultimately benefit from AI. In contrast, we believe standalone point solutions/single -feature products, consumer -facing applications, more content centric -tools, and business models that are more sensitive to seat -based pricing are most likely to face the largest AI-related challenges . Q: What is HLEND’s exposure to software? A: HLEND’s $25.3 billion investment portfolio as of December 31, 2025 , was comprised of 380 portfolio companies operating across 54 different industries .2 Within the private portfolio, software represented $4.5 billion, or 19% of fair market value . HLEND’s software exposure is highly diversified and primarily targets large, cash flow generating companies with a senior secured $25.3B investment focus and conservative detachment points . Total Portfolio As of December 31, 2025 , 99 .7%3 of HLEND’s private software exposure 19% consists of first lien senior secured loans . We have sought to structure these investments conservatively, with a weighted average loan-to-value of 31%4 as $4.5B of the same date, versus a 39 %4 weighted average loan-to-value at the total Software portfolio level. We believe this provides a meaningful equity cushion, even in scenarios of significant value degradation . Importantly, HLEND’s software portfolio is predominantly a newer vintage, with 83 % of loans originated in 2024 and 2025 . We believe this positioning helped us avoid the leverage excesses that characterized the 2019–2021 pre-rate hiking cycle . REPRESENTS HPS’S SUBJECTIVE VIEWS AND IS SUBJECT TO CHANGE BASED ON MARKET ENVIRONMENT

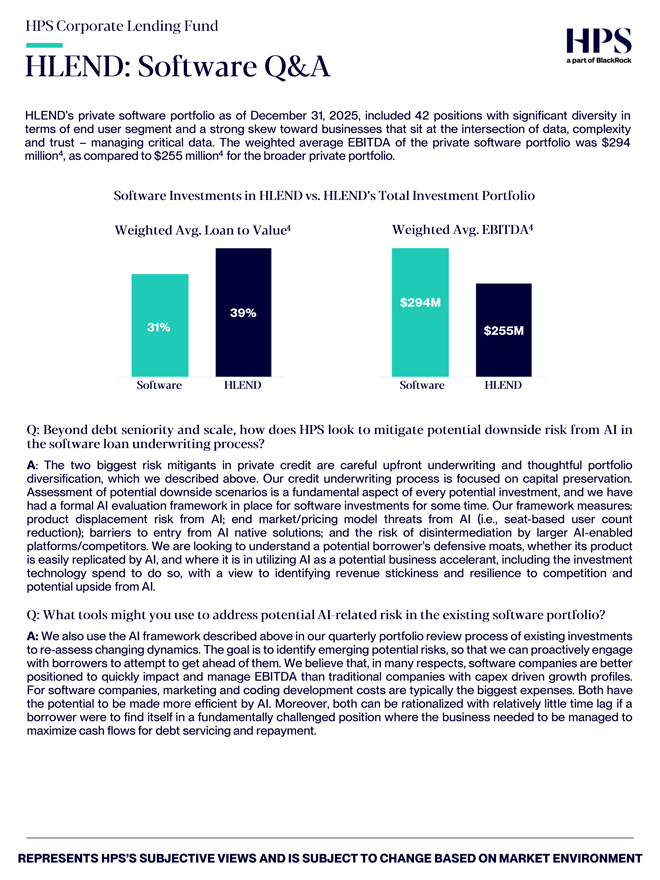

HPS Corporate Lending Fund HLEND: Software Q&A HLEND’s private software portfolio as of December 31, 2025 , included 42 positions with significant diversity in terms of end user segment and a strong skew toward businesses that sit at the intersection of data, complexity and trust – managing critical data. The weighted average EBITDA of the private software portfolio was $294 million4, as compared to $255 million4 for the broader private portfolio. Software Investments in HLEND vs. HLEND’s Total Investment Portfolio Weighted Avg. Loan to Value 4 Weighted Avg. EBITDA 4 $294M 39% 31% $255M Software HLEND Total Software HLEND Total Q: Beyond debt seniority and scale, how does HPS look to mitigate potential downside risk from AI in the software loan underwriting process? A : The two biggest risk mitigants in private credit are careful upfront underwriting and thoughtful portfolio diversification, which we described above . Our credit underwriting process is focused on capital preservation . Assessment of potential downside scenarios is a fundamental aspect of every potential investment, and we have had a formal AI evaluation framework in place for software investments for some time. Our framework measures : product displacement risk from AI; end market/pricing model threats from AI (i.e., seat -based user count reduction) ; barriers to entry from AI native solutions ; and the risk of disintermediation by larger AI-enabled platforms/competitors . We are looking to understand a potential borrower’s defensive moats, whether its product is easily replicated by AI, and where it is in utilizing AI as a potential business accelerant, including the investment technology spend to do so, with a view to identifying revenue stickiness and resilience to competition and potential upside from AI. Q: What tools might you use to address potential AI -related risk in the existing software portfolio? A : We also use the AI framework described above in our quarterly portfolio review process of existing investments to re-assess changing dynamics . The goal is to identify emerging potential risks, so that we can proactively engage with borrowers to attempt to get ahead of them. We believe that, in many respects, software companies are better positioned to quickly impact and manage EBITDA than traditional companies with capex driven growth profiles . For software companies, marketing and coding development costs are typically the biggest expenses . Both have the potential to be made more efficient by AI. Moreover, both can be rationalized with relatively little time lag if a borrower were to find itself in a fundamentally challenged position where the business needed to be managed to maximize cash flows for debt servicing and repayment . REPRESENTS HPS’S SUBJECTIVE VIEWS AND IS SUBJECT TO CHANGE BASED ON MARKET ENVIRONMENT

HPS Corporate Lending Fund Important Disclosures 1 Represents the first lien private credit loans in HLEND’s Software portfolio as of December 31, 2025 . Average all in yields represents gross calculated yield to 3-year take out at close. Yields are calculated using the weighted average calculated yield of investments within each calendar year and are based on the greater of LIBOR (or applicable reference rate) floor or the 3-year swap rate at the time of close. It is calculated at cost at issuance, and includes expected interest payments . The calculations assume a redemption value of the Implied Cost of Refinancing (as defined below) in year 3, which includes 1) any applicable interest payments owed as a result of the non-call period, which are calculated using the greater of the index floor and the applicable swap rate, plus the at close spread, and 2) any applicable call premium. The foregoing factors, as well as defaults, prepayments, actual changes in base rates and other events would change actual returns, and in some cases, materially so. “Implied Cost of Refinancing” represents the implied weighted average cost of refinancing in each year, given the non-call period(s) and call premium(s) of applicable investments within the stated fund, weighted by the fund’s commitment to said investments. For the first year following investment close, assumes 0.5 years of interest is paid prior to refinancing. Implied cost of refinancing includes 1) any applicable interest payments owed as a result of the non-call period, which are calculated using the greater of the index floor and the applicable swap rate, plus the at close spread, and 2) any applicable call premium. Excludes investments where the concept of call protection is not applicable, such as equity or equity-like positions and certain portfolio of receivables or investments structured with a minimum multiple-on-invested-capital provision. For the purposes of the weighted average calculation, investments with a non-call life provision are treated as having a non-call period of the maturity date less close date (in years), investments without a non-call period are treated as having a 0 non-call period, and investments without call premium are treated as having par call premium. HLEND all in yield is estimated, takes into account the upfront fee, is calculated at cost, and includes interest payments and does not reflect management and incentive fees, financing costs and other applicable fund and account expenses . Defaults, prepayments and other events may change returns significantly. Calculated yields are for illustrative purposes only and are not a representation of actual performance . 2 Based on MSCI / S&P Global Industry Classification Standard (“GICS”) industry definition. 3 Includes “last out” portions of first lien senior secured loans. 4 Calculated with respect to all level 3 investments (or, with respect to weighted average loan to value, all level 3 debt investments) in the Software Industry based on MSCI / S&P Global Industry Classification Standard (“GICS”) industry definition in the investment portfolio for which fair value is determined by the Investment Adviser (in its capacity as the investment adviser of HLEND, with assistance, at least quarterly, from a third-party valuation firm, and overseen by HLEND’s Board of Trustees), and excludes quoted assets and investments in joint ventures. In the case of weighted average EBITDA only, excludes investments with no reported EBITDA or where EBITDA, in the Investment Adviser’s judgement made in its discretion, was not a material component of the original investment thesis, such as loan-to-value-based loans, NAV-based loans or reorganized equity. Weighted average EBITDA is weighted based on the fair value of the total applicable level 3 investments. Loan to value is calculated as net debt through each respective investment tranche in which HLEND holds an investment divided by enterprise value or value of underlying collateral of the portfolio company. Weighted average loan to value is weighted based on the fair value of the total applicable level 3 debt investments. Excludes investments on non-accrual status as of December 31, 2025 . Figures are derived from the most recent financial statements from portfolio companies. Important Disclosures The contents of this communication: (i) do not constitute an offer of securities or a solicitation of an offer to buy securities, (ii) offers can be made only by the respective offering documents which are available upon request, (iii) do not and cannot replace the offering documents and is qualified in its entirety by the offering documents, and (iv) may not be relied upon in making an investment decision related to any investment offering by HLEND . All potential investors must read the offering documents and no person may invest without acknowledging receipt and complete review of offering documents . With respect to any “targeted” goals outlined herein, these do not constitute a promise of performance, nor is there any assurance that the investment objectives of any program will be attained. All investments carry the risk of loss of some or all of the principal invested. These “targeted” factors are based upon reasonable assumptions more fully outlined in the offering documents for the respective investment opportunity. Consult the offering documents for investment conditions, risk factors, minimum requirements, fees and expenses and other pertinent information with respect to any investment. Past performance is no guarantee of future results. All information is subject to change . You should always consult a tax and/or finance professional prior to investing. HLEND does not warrant the accuracy or completeness of the information contained herein. Securities offered through HPS Securities, LLC Member: FINRA/SIPC . HPS Securities, LLC is an affiliate of HPS Investment Partners, LLC and HPS Advisors, LLC . Forward Looking Statement Disclosure Certain information contained in this document constitutes “forward looking statements,” which can be identified by the use of forward looking terminology such as “may,” “will,” “expect,” “ intend,” “anticipate,” “estimate,” “believe,” “continue” or other similar words, or the negatives thereof. These may include HLEND’s financial projections and estimates and their underlying assumptions, statements about plans, objectives and expectations with respect to future operations, and statements regarding future performance . Such forward-looking statements are inherently uncertain and there are or may be important factors that could cause actual outcomes or results to differ materially from those indicated in such statements. HLEND believes these factors include but are not limited to those described under the section entitled “Risk Factors” in its prospectus and any such updated factors included in its periodic filings with the Securities and Exchange Commission (the “SEC”) which will be accessible on the SEC’s website at www.sec .gov. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in HLEND’s prospectus and other filings. Except as otherwise required by federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future developments or otherwise. Index Definitions The MSCI / S&P Global Industry Classification Standard (“GICS”) is an industry classification taxonomy launched by MSCI and S&P in 1999. The GICS uses a system of 11 sectors, partitioned into 25 industry groups, which are further divided into 74 industries, which then contain 163 subindustries . REPRESENTS HPS’S SUBJECTIVE VIEWS AND IS SUBJECT TO CHANGE BASED ON MARKET ENVIRONMENT

HPS Corporate Lending Fund Important Disclosures Summary of Risk Factors HPS Corporate Lending Fund (“HLEND” or the “Fund”) is a non-exchange traded business development company (“BDC”) that invests at least 80 % of its total assets (net assets plus borrowings for investment purposes) in private credit investments (bonds and other credit instruments that are issued in private offerings or issued by private companies) . This investment involves a high degree of risk. You should purchase these securities only if you can afford the complete loss of your investment. You should read the prospectus carefully for a description of the risks associated with an investment in HLEND . These risks include, but are not limited to, the following: • HLEND has a limited operating history and there is no assurance that HLEND will achieve HLEND’s investment objectives . • You should not expect to be able to sell your shares regardless of how HLEND performs. • You should consider that you may not have access to the money you invest for an extended period of time. • HLEND does not intend to list its shares on any securities exchange, and HLEND does not expect a secondary market in HLEND shares to develop prior to any listing. • Because you may be unable to sell your shares, you will be unable to reduce your exposure in any market downturn. • HLEND has implemented a share repurchase program, but only a limited number of shares will be eligible for repurchase and repurchases will be subject to available liquidity and other significant restrictions. • An investment in HLEND’s Common Shares is not suitable for you if you need access to the money you invest. See “Suitability Standards” and “Share Repurchase Program” in the prospectus . • You will bear substantial fees and expenses in connection with your investment. See “Fees and Expenses” in the prospectus . • HLEND cannot guarantee that HLEND will make distributions, and if HLEND does, HLEND may fund such distributions from sources other than cash flow from operations, including, without limitation, the sale of assets, borrowings, return of capital or offering proceeds, and HLEND has no limits on the amounts HLEND may pay from such sources . A return of capital (1) is a return of the original amount invested, (2) does not constitute earnings or profits and (3) will have the effect of reducing the basis such that when a shareholder sells its shares the sale may be subject to taxes even if the shares are sold for less than the original purchase price. • Distributions may also be funded in significant part, directly or indirectly, from temporary fee waivers or expense reimbursements borne by the Adviser or its affiliates, that may be subject to reimbursement to the Adviser or its affiliates. The repayment of any amounts owed to HLEND’s affiliates will reduce future distributions to which you would otherwise be entitled. • HLEND uses and continues to expect to use leverage, which will magnify the potential for loss on amounts invested and may increase the risk of investing in HLEND . The risks of investment in a highly leveraged fund include volatility and possible distribution restrictions. • HLEND intends to invest primarily in securities that are rated below investment grade by rating agencies or that would be rated below investment grade if they were rated. Below investment grade securities, which are often referred to as “junk,” have predominantly speculative characteristics with respect to the issuer’s capacity to pay interest and repay principal. They may also be illiquid and difficult to value. REPRESENTS HPS’S SUBJECTIVE VIEWS AND IS SUBJECT TO CHANGE BASED ON MARKET ENVIRONMENT